The government has been relentlessly focusing on mainstreaming the growth of MSMEs, more importantly, after the MSME Development Act 2006 was enacted. On 9 May 2007, the Ministry of Small-Scale Industries (SSI) and the Ministry of Agro and Rural Industries were merged to form the Ministry of Micro, Small, and Medium Enterprises (MSME). It now designs policies and promotes/facilitates programs, projects, and schemes, and monitors their implementation to assist MSMEs and help them to scale up. The results of the collaborative efforts of stakeholders are evident from the way MSME has thrived in the last few years. But its potentiality is yet to be fully harnessed to pump prime growth.

Besides many initiatives, three thrust areas are prominent: (i) enhancing access to affordable finance; (ii) ensuring access to state-of-the-art technology; and (iii) increasing access to extensive and expansive domestic and global markets. MSMEs are complementary to large industries as ancillary units, and this sector contributes significantly to inclusive industrial development. The MSMEs are expanding their domain across sectors of the economy, producing a diverse range of products and services to meet the demands of domestic as well as global markets. The cluster of MSMEs is vibrant to increase its outreach in scale and dimensions.

- Increasing Role of MSME Sector:

The quantitative presence of MSMEs will be able to explain their increasing role in the economy. The latest data suggests that 63.4 million MSME units are operating, of which 20 million units are in manufacturing, 23 million are in Trade, and 20.4 million are in other services. Out of them, 35.3 million are registered in the Udyam portal, forming 57 percent of the total number of units. The rest are yet to get covered. Again, geographical distribution indicates 32.5 million units are in rural areas, whereas 30.9 million are located in urban areas.

As far as ownership is concerned, it is male-dominated, with 80 percent of MSME units owned by men and 20 percent by women. The MSME sector employs close to 111 million people – 36 million working in manufacturing, 39 million in trade, and 36 million in other sectors. The sector contributed close to 44 percent of the Gross Value Added (GVA) in March 2023, and its share in the exports works out to 43.59 percent.

MSMEs contribute nearly 30 percent of GDP, 45 percent of the manufacturing output, and 46 percent of exports in fiscal year 2024. By 2047, the manufacturing and services sector is projected to employ 67 percent of the workforce and contribute over 75 percent of the GDP.

- Policy initiatives:

Looking at the potential of the MSME sector, several policy measures have been initiated. A national manufacturing mission is launched to further the ‘Make in India’. Incidentally, it can help take advantage of the China+1 strategy of many countries. India is well geared up to serve as a manufacturing hub for many countries.

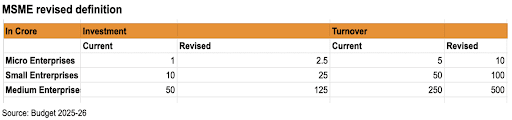

In the Union Budget 2025-26, the definition of various units has been proposed to be raised, which will now be made effective from April 1, 2025, widening the scope for obtaining finance and support from the government.

The MSME credit card limit has been raised from Rs 5 lakhs to Rs 10 lakhs. The credit guarantee cover for micro and small enterprises (MSEs) has been enhanced from Rs. 5 crores to Rs. 10 crores, unlocking an estimated Rs. 1.5 lakh crore in additional credit over the next 5 years.

A new Rs.. 10,000 crore fund of funds (FOF) has been established to provide financial support to start-ups across various sectors. These funds aim to enhance access to capital, enabling startups to scale up their operations and drive innovation. Another MSME scheme is rolled out to assist 5 lakh first-time entrepreneurs from the SC, ST, and women categories over the next 5 years with a built-in term loan of up to Rs. 2 crores. The loan limit under the PMSVANidhi scheme for street vendors has been increased from Rs. 10,000 to Rs. 30,000 to be delivered through the UPI app and is expected to benefit close to 68 lakh street vendors. Promotion of private sector research with an outlay of Rs. 20000 crores, export promotion, ease of doing business, and introduction of Bbarat Trade Net (BTN) to facilitate international trade are the other measures to boost the sector.

The recently launched PM Vishwakarma Scheme, with its objective of providing end-to-end support to artisans and craftspeople of 18 traditional trades, definitely has its roots in Welfare Economics. It promises to maximize public welfare with inclusion and public participation. The Scheme is well-nuanced, futuristic, and comprehensively covers all three crucial aspects to harness the power of skilled youth.

- Challenges of the MSME sector:

While technology obsolescence, lack of funds for technology upgradation, inadequate digital and financial literacy, lack of adequate marketing support for MSME products, and continued skill gaps in traditional entrepreneurial activities continue to pose daunting risks to the sector. But, beyond these, the credit shortfall of close to Rs 25 – 30 lakh crores is the main constraint for the sector to grow to its potential. Despite improved credit risk assessment systems, an array of collateral-free loans, MUDRA loan schemes, and expanded credit guarantees for MSME units, formal lending institutions are not able to provide adequate credit. NBFCs, including Fintech, are pitching in to bridge the gap, but the sector is struggling to get funding to expand.

The recent data indicate that credit to MSMEs grew by 5.8 percent in FY23, 8.5 percent in FY24, and 7.9 percent in H1 of FY25. The corresponding industry credit growth was 15 percent, 20.2 percent, and 11.5 percent. The outstanding bank credit to MSME was Rs. 33.66 trillion, Rs. 36.52 trillion, and Rs. 37.74 trillion out of the total outstanding bank credit of Rs. 136.75 trillion, Rs. 164.32 trillion, and Rs. 172.38 trillion during the same period. The number of MSME credit accounts of SCBs increased during 2023-24, reversing the trend during the period 2020-21 to 2022-23.

The flow of credit to MSMEs is not accelerating at the desired pace to harness the full potential of the sector. Low ticket size, high transaction cost, and inability to monitor the MSME loan portfolio to maintain the asset quality are some of the constraints of banks.

With interoperable technology and possible centralisation of loan processing on a hub and spokes model operating on assembly line principles, there is some improvement in the delivery of credit to the sector. Dissemination of financial and digital literacy, spread of MSME touch points by galvanising the business correspondent model, skill development, and support for marketing of products can provide the much-needed impetus.

Disclaimer

Views expressed above are the author's own.

Top Comment

{{A_D_N}}

{{C_D}}

{{{short}}} {{#more}} {{{long}}}... Read More {{/more}}

{{/totalcount}} {{^totalcount}}Start a Conversation